Discover how to create a personalized financial wellness strategy tailored to your unique goals, circumstances, and values for long-term success.

Financial wellness isn’t a one-size-fits-all concept. Just as each person has unique health needs, your financial wellness journey requires a personalized approach tailored to your specific circumstances, goals, and life stage. In today’s rapidly evolving financial landscape, understanding how to create and maintain a personalized financial wellness strategy has become more critical than ever.

Table of Contents

What Is Personalized Financial Wellness?

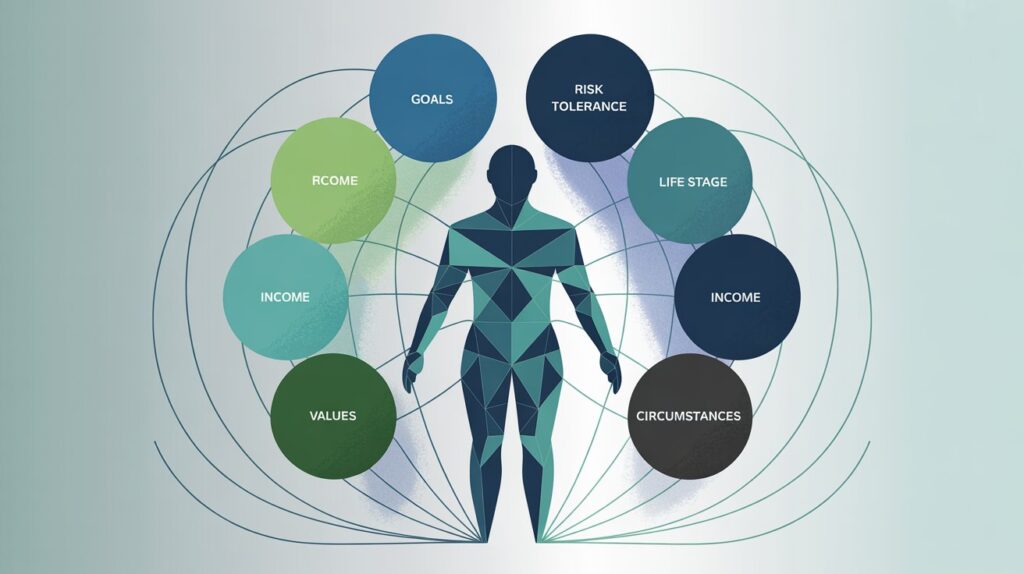

Personalized financial wellness goes beyond basic budgeting or investment advice. It’s a holistic approach that considers your individual financial situation, emotional relationship with money, life goals, and personal circumstances to create a comprehensive strategy for financial health and security.

Unlike generic financial advice, personalized financial wellness takes into account factors such as your income patterns, family obligations, risk tolerance, career trajectory, and even your cultural background and values around money. This individualized approach recognizes that what works for one person may not work for another, even if their financial situations appear similar on the surface.

The concept has gained significant traction in recent years. According to research from PwC’s Employee Financial Wellness Survey, companies are increasingly recognizing the need to personalize financial wellness benefits to employee life and career stages, connecting with employees where they are comfortable and acknowledging that even small, incremental improvements can lead to significant benefits in productivity and engagement.

The Growing Importance of Financial Wellness in 2025

The financial wellness landscape has experienced remarkable growth and transformation. Market research indicates that the U.S. financial wellness benefits market was valued at $587.02 million in 2023 and is projected to reach $1.21 billion by 2029, rising at a compound annual growth rate of 12.91%.

This explosive growth reflects a fundamental shift in how individuals and organizations view financial health. The pandemic, economic uncertainty, and changing work patterns have highlighted the critical connection between financial wellness and overall well-being. Companies are recognizing that employees’ financial stress directly impacts their productivity, engagement, and job satisfaction.

The Role of Technology in Personalization

Modern financial wellness programs leverage digital platforms and data analytics to deliver truly personalized experiences. These technological advances enable real-time assessment of financial behaviors, customized educational content, and adaptive recommendations that evolve with changing circumstances.

Research shows that technology integration and personalization enhance the effectiveness of financial wellness programs, with employers leveraging digital platforms and personalized solutions to meet diverse employee needs and preferences.

Core Components of Personalized Financial Wellness

1. Comprehensive Financial Assessment

The foundation of any personalized financial wellness plan begins with a thorough assessment of your current financial situation. This goes beyond simply calculating net worth or monthly cash flow. A comprehensive assessment includes:

Income Analysis: Understanding not just how much you earn, but the stability and predictability of your income streams. This is particularly important for freelancers, commission-based workers, or those with variable income.

Expense Categorization: Breaking down expenses into needs versus wants, fixed versus variable costs, and identifying patterns in spending behavior that may not be immediately obvious.

Debt Evaluation: Analyzing not just the amount of debt, but the types, interest rates, payment terms, and the emotional impact of debt on your overall well-being.

Asset Assessment: Reviewing all assets, including traditional investments, retirement accounts, real estate, and even non-traditional assets like business equity or intellectual property.

2. Goal Setting and Prioritization

Personalized financial wellness requires clear, specific, and measurable goals that align with your values and life circumstances. These goals should be:

Time-Bound: Short-term (1 year), medium-term (2-5 years), and long-term (5+ years) objectives that work together cohesively.

Values-Aligned: Goals that reflect what’s truly important to you, whether that’s early retirement, funding children’s education, starting a business, or supporting family members.

Realistic and Achievable: Objectives that stretch you without being so ambitious that they lead to frustration and abandonment of the plan.

3. Risk Assessment and Management

Understanding your risk tolerance is crucial for personalized financial wellness. This includes both your emotional comfort with risk and your financial capacity to handle potential losses. Effective risk management involves:

Insurance Planning: Ensuring adequate coverage for health, disability, life, and property without over-insuring or leaving dangerous gaps.

Emergency Fund Strategy: Building and maintaining emergency reserves appropriate to your income stability, family obligations, and comfort level.

Investment Risk Alignment: Matching investment strategies to both your risk tolerance and time horizon for various goals.

Creating Your Personalized Financial Wellness Strategy

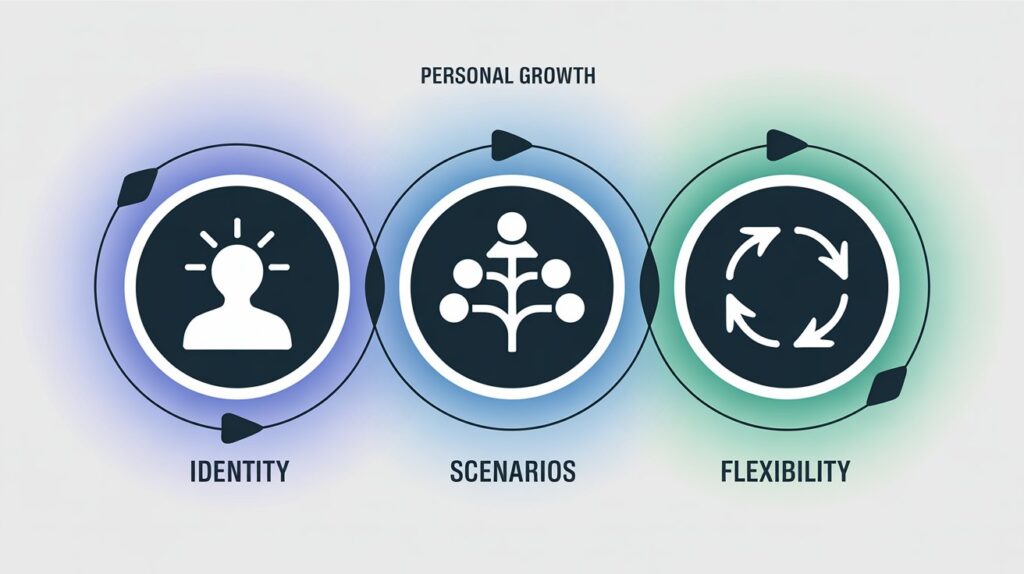

Step 1: Define Your Financial Identity

Before diving into specific strategies, take time to understand your financial identity. This includes your money mindset, learned behaviors around money, and cultural influences that shape your financial decisions.

Consider questions like: How do you feel when making financial decisions? What money lessons did you learn growing up? What are your deepest fears and greatest hopes related to money? Understanding these underlying factors helps create a sustainable approach to financial wellness.

Step 2: Develop Multiple Scenarios

Life is unpredictable, so your personalized financial wellness plan should account for various scenarios. Create financial plans for:

Best-Case Scenarios: What would you do if your income increased significantly, you received an inheritance, or your investments performed exceptionally well?

Worst-Case Scenarios: How would you handle job loss, health issues, market downturns, or family emergencies?

Most Likely Scenarios: Base-case planning for steady progression toward your goals with normal life changes and challenges.

Step 3: Build in Flexibility and Regular Reviews

A truly personalized financial wellness plan evolves with your life. Build in regular review periods (quarterly or semi-annually) to assess progress, adjust goals, and adapt strategies based on changing circumstances.

The Psychology of Personalized Financial Wellness

Understanding the psychological aspects of money management is crucial for long-term success. Financial behavior is often driven by emotions, past experiences, and unconscious biases rather than purely rational decision-making.

Behavioral Finance Considerations

Decision Fatigue: Making too many financial decisions can lead to poor choices later. Automate routine decisions where possible to preserve mental energy for important choices.

Loss Aversion: People typically feel the pain of losses more acutely than the pleasure of equivalent gains. Factor this into investment strategies and goal-setting approaches.

Present Bias: The tendency to prioritize immediate rewards over future benefits can sabotage long-term financial wellness. Use techniques like automatic savings and visual goal tracking to overcome this bias.

Building Positive Financial Habits

Sustainable financial wellness relies on developing positive habits rather than relying on willpower alone. Focus on:

Gradual Implementation: Introduce new financial behaviors slowly to increase the likelihood of long-term adoption.

Environmental Design: Structure your financial environment to make good choices easier and bad choices harder.

Social Support: Engage with others who share similar financial values and goals to maintain motivation and accountability.

Technology Tools for Personalized Financial Wellness

Modern technology offers unprecedented opportunities for personalizing financial wellness strategies. From AI-powered budgeting apps to robo-advisors that adjust portfolios based on life changes, technology can provide real-time insights and automated adjustments to keep you on track.

Digital Financial Wellness Platforms

Many platforms now offer comprehensive financial wellness tools that integrate budgeting, investment management, retirement planning, and educational resources. These platforms use data analytics to provide personalized recommendations and track progress toward multiple goals simultaneously.

Research from Enrich shows that digital financial wellness programs can impact real-world behavior changes, with measurable improvements in emergency savings, retirement plan participation, financial stress levels, and credit scores over a 12-month period.

Artificial Intelligence and Machine Learning

AI-powered tools can analyze spending patterns, predict cash flow needs, and suggest optimizations to your financial strategy. These tools learn from your behavior and preferences to provide increasingly personalized recommendations over time.

Working with Financial Professionals

While technology tools are valuable, working with qualified financial professionals remains important for comprehensive financial wellness. The key is finding advisors who understand and embrace personalized approaches rather than applying cookie-cutter solutions.

Choosing the Right Advisory Relationship

Look for financial advisors who:

Take Time to Understand You: The best advisors invest significant time in understanding your unique circumstances, goals, and preferences before making recommendations.

Offer Comprehensive Services: Consider working with firms that provide integrated services including investment management, tax planning, and insurance solutions to ensure all aspects of your financial life work together cohesively.

Embrace Technology: Modern advisory relationships should leverage technology to provide better service, more frequent communication, and enhanced portfolio management.

The Family Office Approach

For families with more complex financial situations, the family office approach provides the highest level of personalized service. This comprehensive approach, traditionally available only to ultra-high-net-worth families, is becoming more accessible to a broader range of clients who value integrated, personalized financial services.

Measuring Success in Personalized Financial Wellness

Success in financial wellness isn’t just about accumulating wealth. A truly successful personalized financial wellness strategy should improve multiple aspects of your life:

Quantitative Measures

Progress Toward Goals: Regular measurement of advancement toward specific financial objectives.

Net Worth Growth: Tracking overall financial position over time, adjusted for life stage and economic conditions.

Cash Flow Improvement: Monitoring the balance between income and expenses, with particular attention to discretionary spending capacity.

Risk Management: Assessing whether your insurance coverage and emergency reserves remain adequate as your situation changes.

Qualitative Measures

Reduced Financial Stress: Decreased anxiety about money matters and increased confidence in financial decision-making.

Improved Financial Behaviors: Development of positive habits around spending, saving, and investing.

Enhanced Life Satisfaction: Greater alignment between financial resources and personal values and goals.

Increased Financial Knowledge: Growing understanding of financial concepts and improved ability to make informed decisions.

Common Challenges and Solutions

Challenge 1: Information Overload

With countless financial products, strategies, and advice sources available, many people feel overwhelmed when trying to create a personalized approach.

Solution: Focus on your specific goals and circumstances rather than trying to implement every strategy you encounter. Work with qualified professionals who can help filter information and identify what’s most relevant to your situation.

Challenge 2: Changing Life Circumstances

Life changes like marriage, divorce, job changes, health issues, or economic shifts can disrupt even well-planned financial strategies.

Solution: Build flexibility into your plan from the beginning. Expect change and create systems for regularly reviewing and adjusting your strategy. Maintain emergency reserves and avoid over-committing to inflexible financial products.

Challenge 3: Behavioral Consistency

Many people understand what they should do financially but struggle to maintain consistent behaviors over time.

Solution: Focus on systems and automation rather than relying on willpower. Create environmental supports that make good financial choices easier and establish accountability mechanisms through technology or professional relationships.

The Future of Personalized Financial Wellness

As we look toward the future, several trends are shaping the evolution of personalized financial wellness:

Increased Integration

Financial wellness is becoming more integrated with overall health and wellness programs. Companies are recognizing the interconnections between financial, physical, and mental health, leading to more holistic approaches to employee well-being.

Enhanced Personalization

Advances in data analytics and artificial intelligence will enable even more sophisticated personalization, with financial strategies that adapt in real-time to changing circumstances and behaviors.

Expanded Access

Technology is democratizing access to sophisticated financial wellness tools and strategies that were previously available only to high-net-worth individuals. This trend is expected to continue, making personalized financial wellness more accessible to people at all income levels.

Taking Action: Your Next Steps

Creating a personalized financial wellness plan may seem daunting, but the key is to start where you are and take incremental steps toward improvement. Here’s how to begin:

- Conduct an Honest Financial Assessment: Take stock of your current situation without judgment. Understanding where you are is essential for determining where you want to go.

- Clarify Your Values and Goals: Spend time reflecting on what’s truly important to you and how financial wellness can support those priorities.

- Start Small: Choose one or two areas for initial focus rather than trying to overhaul everything at once. Success in small areas builds momentum for larger changes.

- Seek Professional Guidance: Consider working with qualified financial professionals who can provide objective perspectives and specialized expertise.

- Embrace the Journey: Remember that financial wellness is an ongoing process, not a destination. Be patient with yourself and maintain focus on long-term progress rather than short-term perfection.

Personalized financial wellness represents a fundamental shift from generic financial advice to customized strategies that reflect your unique circumstances, values, and goals. By embracing this personalized approach, you can create a financial foundation that not only builds wealth but also supports your overall well-being and life satisfaction.

The investment in creating a truly personalized financial wellness strategy pays dividends far beyond mere financial returns. It provides peace of mind, reduces stress, and creates the foundation for living life on your own terms. In our increasingly complex financial world, this personalized approach isn’t just beneficial—it’s essential for long-term financial success and life satisfaction.

Frequently Asked Questions

How often should I review my personalized financial wellness plan? Review your plan quarterly for minor adjustments and annually for comprehensive evaluation. Major life changes may require immediate plan updates.

Can I create a personalized financial wellness plan on my own? While self-directed planning is possible, working with qualified professionals often provides valuable objectivity, expertise, and accountability that improve outcomes.

What’s the biggest mistake people make with financial wellness planning? The most common mistake is trying to implement too many changes at once. Sustainable financial wellness comes from gradual, consistent improvements rather than dramatic overhauls.

How do I know if my financial wellness plan is working? Success should be measured both quantitatively (progress toward goals, improved cash flow) and qualitatively (reduced stress, increased confidence). Regular monitoring of both aspects is important.

What role does technology play in personalized financial wellness? Technology enables more sophisticated analysis, automation of routine tasks, and real-time adjustments to your strategy. However, technology should supplement, not replace, thoughtful planning and professional guidance when needed.