Discover how SECURE Act 2.0’s automatic enrollment, catch-up contributions, and RMD changes are helping millions build better retirement savings in 2025.

Table of Contents

How SECURE Act 2.0 Is Revolutionizing American Retirement Savings: A Complete Guide for 2025

The American retirement crisis has been brewing for decades. With traditional pensions disappearing and Social Security facing uncertainty, millions of workers have struggled to save enough for their golden years. Enter the SECURE Act 2.0 – a comprehensive piece of legislation that’s quietly transforming how Americans approach retirement planning.

Since becoming law on December 29, 2022, the SECURE Act 2.0 has introduced over 90 new provisions designed to expand retirement plan access and boost savings. But the real question isn’t what changes the law brings – it’s whether these changes are actually helping everyday Americans build the retirement security they desperately need.

The early indicators are promising. According to the Employee Benefit Research Institute, the percent of American workers participating in employment-based retirement plans has increased from around 31.6% in 2018 to around 48.9 percent in 2022. This dramatic jump suggests that the groundwork laid by the original SECURE Act, combined with SECURE 2.0’s enhancements, is beginning to pay dividends for American workers.

Understanding the SECURE Act 2.0 Foundation

The Setting Every Community Up for Retirement Enhancement (SECURE) Act 2.0 builds upon its 2019 predecessor, addressing critical gaps in America’s retirement system. While the original SECURE Act focused primarily on expanding access to retirement plans, SECURE 2.0 takes a more comprehensive approach by tackling participation rates, contribution limits, and withdrawal flexibility.

According to one study, by 2050, the U.S. will face a $137 trillion retirement income gap – the difference between what savers should have and what they’ve actually saved. This staggering figure underscores why legislative action was necessary to help Americans catch up on their retirement savings goals.

The new law recognizes that traditional approaches to retirement saving – relying on employees to voluntarily opt into plans and make contribution decisions – simply aren’t working for millions of Americans. Instead, SECURE 2.0 embraces behavioral economics principles, using automatic features and enhanced incentives to make saving for retirement the default choice rather than an active decision.

Automatic Enrollment: Making Retirement Savings the Default Choice

Perhaps the most significant change under SECURE Act 2.0 is the mandatory automatic enrollment requirement for new retirement plans. Starting with plan years beginning on or after January 1, 2025, all new 401(k) and 403(b) plans must automatically enroll eligible employees.

This isn’t just a minor administrative change – it’s a fundamental shift in how retirement saving works. Under the old system, employees had to actively choose to join their company’s retirement plan, often during busy onboarding periods when they were overwhelmed with new information. Research consistently shows that this “opt-in” approach leads to lower participation rates, particularly among younger workers and those with lower incomes.

The automatic enrollment requirement includes several key protections for employees:

- Workers can still opt out if they choose

- Initial contribution rates must be between 3% and 10% of pre-tax earnings

- Plans must include automatic escalation features that gradually increase contributions over time

- Employees retain full control over their contribution levels and investment choices

Small employers aren’t left behind in this transition. Church plans, government-sponsored plans, and employers with fewer than 10 employees are exempt from the automatic enrollment requirement, recognizing the administrative burden these features can place on smaller organizations.

Enhanced Catch-Up Contributions for Near-Retirees

One of SECURE Act 2.0’s most valuable provisions addresses a critical problem: workers who are nearing retirement but haven’t saved enough. The law significantly expands catch-up contribution opportunities for Americans aged 60-63, recognizing that these are often peak earning years when workers have the greatest capacity to accelerate their retirement savings.

If you’re age 60 to 63, you can already make catch-up contributions to your retirement accounts, but SECURE 2.0 ups the total by quite a lot: $11,250 to a 401(k) or 403(b), or $5,250 to an IRA in 2025. This represents a substantial increase from previous limits and provides a meaningful opportunity for workers to make up for lost time.

Consider Sarah, a 62-year-old marketing manager who started focusing seriously on retirement planning only five years ago. Under the old rules, she could contribute $23,000 to her 401(k) plus a $7,500 catch-up contribution, for a total of $30,500 annually. Under SECURE 2.0, Sarah can now contribute up to $34,750 annually – an extra $4,250 that can make a significant difference in her retirement security.

The enhanced catch-up contributions are particularly valuable because they come during what financial planners call the “wealth accumulation sweet spot” – the years when many workers have paid off major expenses like mortgages and children’s college costs, freeing up income for retirement savings.

Required Minimum Distribution Changes: More Time to Grow Your Savings

SECURE Act 2.0 also provides significant relief when it comes to required minimum distributions (RMDs), the mandatory withdrawals that retirees must begin taking from their retirement accounts. SECURE 2.0 increases the age for required minimum distributions (RMDs) to 73, beginning on January 1, 2023, and to age 75 on January 1, 2033.

This change might seem incremental, but it can have a substantial impact on retirement outcomes. Every year that retirement savings can remain invested and growing represents additional compound growth potential. For someone with $500,000 in retirement savings earning a 7% annual return, delaying RMDs by two years could result in tens of thousands of additional dollars in retirement wealth.

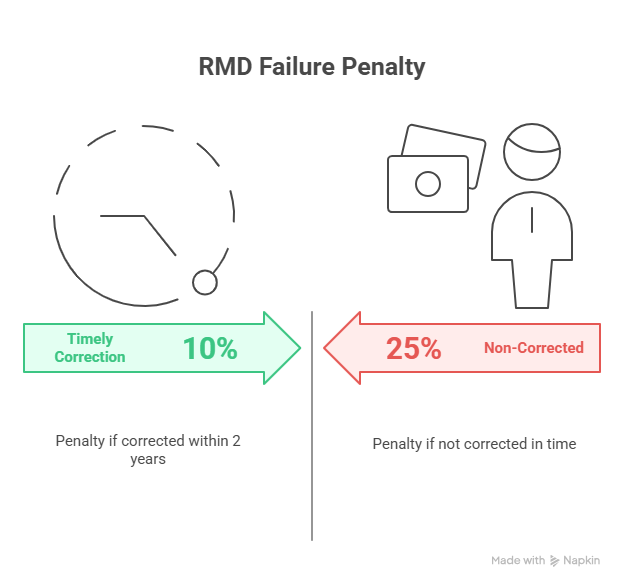

The law also reduces the penalty for failing to take required distributions. The penalty for failing to take an RMD decreased to 25% of the RMD amount, from 50%, and 10% if corrected in a timely manner within 2 years for IRAs. This change acknowledges that RMD mistakes often result from confusion rather than intentional tax avoidance.

Addressing Student Debt: A Modern Retirement Challenge

One of SECURE Act 2.0’s most innovative provisions addresses a uniquely modern challenge: the impact of student loan debt on retirement savings. Many young workers face an impossible choice between paying down educational debt and contributing to retirement plans, often missing out on valuable employer matching contributions.

The new law allows employers to treat student loan payments as elective deferrals for purposes of employer matching contributions. This means that an employee making $50,000 annually who pays $300 monthly toward student loans can receive employer matching contributions as if they were contributing that $300 to their 401(k).

This provision recognizes the reality facing millions of Americans: student loan debt that delays traditional milestones like homeownership and retirement saving. By allowing student loan payments to trigger employer matches, SECURE 2.0 ensures that debt-burdened workers don’t miss out entirely on retirement savings during their crucial early career years.

Emergency Savings: Building Financial Resilience

SECURE Act 2.0 introduces several provisions designed to help Americans build emergency savings while continuing to save for retirement. The law allows penalty-free withdrawals of up to $1,000 annually for emergency expenses, providing a safety net that can prevent workers from raiding their retirement accounts for unexpected costs.

The legislation also permits plans to include personal savings account features, allowing employees to contribute up to $2,500 annually to an emergency fund through payroll deduction. These contributions can earn employer matching, helping workers build the short-term savings that financial experts recommend while still preparing for retirement.

These emergency savings provisions address a critical barrier to retirement plan participation. Many workers avoid contributing to retirement accounts because they fear they won’t be able to access their money in case of emergency. By providing controlled access to funds for genuine emergencies, SECURE 2.0 makes retirement saving less intimidating for workers living paycheck to paycheck.

Small Business Incentives: Expanding Access Through Tax Credits

Small businesses have historically been less likely to offer retirement plans due to cost and administrative complexity. SECURE Act 2.0 addresses this challenge with significantly enhanced tax credits for small employers who establish new retirement plans.

The SECURE Act 2.0 increases this credit to 100 percent of qualified start-up costs for employers with up to 50 employees. This means that qualifying small businesses can receive dollar-for-dollar tax credits for their retirement plan setup and administrative costs, dramatically reducing the financial barrier to plan establishment.

The law also provides additional credits for employer matching contributions, creating ongoing incentives for small businesses to not only establish plans but to contribute meaningfully to their employees’ retirement security. These credits phase down over five years, providing predictable support during the crucial early years of plan operation.

Real-World Impact: Success Stories and Data

The measurable impact of SECURE Act 2.0 extends beyond participation statistics. The Federal Reserve’s Survey of Consumer Finances shows that in 2019, the average American’s retirement account balance was around $255,000; by 2022, this amount had risen to $333,000. While market performance certainly contributed to this increase, the expansion of retirement plan access and participation likely played a significant role.

Consider the story of Maria, a 28-year-old teacher whose school district implemented automatic enrollment in their 403(b) plan following SECURE Act guidance. Previously overwhelmed by investment choices and unsure how much to contribute, Maria now saves 6% of her salary automatically, with annual increases built into the system. “I probably would have kept putting it off,” Maria admits. “Having it happen automatically took the decision-making pressure off me.”

2.74 million employees started new jobs in the first half of 2022, and many of those who work for companies without auto-enrollment missed opportunities to begin saving immediately. SECURE 2.0’s automatic enrollment requirements will ensure that future job changers don’t face the same delays in beginning their retirement savings journey.

Challenges and Limitations

Despite its comprehensive approach, SECURE Act 2.0 isn’t a silver bullet for America’s retirement crisis. The law primarily benefits workers who have access to employer-sponsored retirement plans, doing less for the millions of Americans who work for employers that don’t offer such benefits.

Additionally, many of the law’s most significant provisions don’t take effect until 2025, meaning their full impact won’t be felt for several years. The automatic enrollment requirements, enhanced catch-up contributions, and expanded small business incentives all operate on delayed implementation schedules that limit their immediate effectiveness.

The legislation also doesn’t address fundamental economic challenges that make retirement saving difficult for many Americans, such as stagnant wages, rising healthcare costs, and housing affordability. While SECURE 2.0 makes it easier to save for retirement, it can’t solve the underlying problem of workers not having enough discretionary income to save.

Looking Ahead: The Future of Retirement Security

SECURE Act 2.0 represents the most significant expansion of retirement savings opportunities in decades, but it’s likely just the beginning of needed reforms. As the law’s provisions take effect over the coming years, policymakers will undoubtedly watch for areas where additional improvements are needed.

Early indicators suggest that the law’s behavioral economics approach – making saving automatic rather than optional – is proving effective. In 2023, 77% of plans with more than 1,000 participants featured automatic enrollment, and this percentage is likely to grow as SECURE 2.0’s requirements take effect.

The success of SECURE Act 2.0 will ultimately be measured not in legislative provisions or regulatory guidance, but in the retirement security of American workers. If the early trends continue, millions of Americans may find themselves significantly better prepared for retirement than previous generations.

Practical Steps for Workers and Employers

For individual workers, SECURE Act 2.0 presents several immediate opportunities:

Review your retirement plan options: Even if your employer hasn’t implemented automatic enrollment, you can still benefit from increased contribution limits and enhanced catch-up opportunities if you’re eligible.

Consider the student loan provision: If you’re paying student loans and your employer offers this option, you might be able to receive matching contributions without reducing your loan payments.

Plan for RMD changes: If you’re approaching retirement, the delayed RMD requirements give you additional time to let your savings grow and plan your withdrawal strategy.

Take advantage of emergency provisions: The new hardship withdrawal options provide important safety nets, but should be used judiciously to preserve your long-term retirement security.

For employers, particularly small businesses, SECURE 2.0 offers compelling reasons to establish or enhance retirement benefits:

Explore enhanced tax credits: The expanded credits for small businesses can make retirement plan establishment much more affordable than previously possible.

Consider automatic features: Even if not required by law, automatic enrollment and escalation can significantly boost employee participation and satisfaction.

Review student loan matching: This innovative benefit can help attract and retain younger employees while supporting their financial wellness.

Frequently Asked Questions

Q: When do SECURE Act 2.0’s automatic enrollment requirements take effect? A: New retirement plans established after December 29, 2022, must include automatic enrollment features for plan years beginning on or after January 1, 2025.

Q: How much can workers aged 60-63 contribute to retirement accounts under the new rules? A: In 2025, eligible workers can contribute up to $34,750 to 401(k) and 403(b) plans, including enhanced catch-up contributions.

Q: Do the new rules apply to existing retirement plans? A: Most SECURE 2.0 provisions apply to both new and existing plans, though automatic enrollment requirements only apply to plans established after the law’s enactment.

Q: Can employers still choose not to offer retirement plans? A: Yes, SECURE 2.0 doesn’t mandate that employers offer retirement plans, but it provides significant incentives for them to do so, particularly for small businesses.

Q: How do the student loan matching provisions work? A: Employers can treat qualifying student loan payments as elective deferrals for purposes of determining employer matching contributions, allowing debt-paying employees to receive matches without reducing their loan payments.

The SECURE Act 2.0 represents a fundamental shift in American retirement policy, moving from voluntary participation models to systems that make saving automatic and accessible. While challenges remain, the early evidence suggests that this approach is helping more Americans build the retirement security they need. As the law’s provisions continue to roll out over the coming years, its full impact on American retirement outcomes will become clearer – but the initial signs point toward a more secure retirement future for millions of workers.