Learn how HSAs protect against rising healthcare costs. Discover 2025 contribution limits, tax benefits, and HSA investment strategies for retirement.

Table of Contents

Healthcare costs continue to climb at an alarming rate, with HealthView Services research showing that annual healthcare expenses for 65-year-old retirees have increased by 60% since 2011. For many Americans approaching retirement, the prospect of facing potentially unlimited medical expenses creates significant financial anxiety.

However, there’s a powerful financial tool that can help you build a dedicated buffer against these rising costs: the Health Savings Account (HSA). When paired with strategic planning, HSAs offer one of the most effective ways to prepare for both current and future healthcare expenses while providing substantial tax advantages that traditional savings accounts simply can’t match.

Understanding HSAs and Healthcare Cost Management

Health Savings Accounts represent a unique triple-tax advantage that makes them particularly valuable for managing healthcare expenses. Unlike other retirement accounts, HSAs allow you to contribute pre-tax dollars, grow investments tax-free, and withdraw funds tax-free when used for qualified medical expenses.

The beauty of HSAs lies in their flexibility for healthcare cost planning. Whether you’re dealing with routine medical expenses today or preparing for potentially significant healthcare costs in retirement, these accounts adapt to your changing needs throughout different life stages.

The Reality of Rising Healthcare Expenses

Current data paints a sobering picture of healthcare cost trends. According to HealthView Services, healthy couples entering retirement could reasonably expect their healthcare costs to reach $1 million throughout their retirement years. This figure has grown substantially, with healthcare costs rising 65% over just six years.

The Centers for Medicare and Medicaid Services projects healthcare spending to increase by 5.4% annually through 2028, reaching a total cost of $6.2 trillion nationally. For individuals, this translates to consistently rising premiums, deductibles, and out-of-pocket expenses that can quickly erode retirement savings.

HSA Contribution Limits and Tax Advantages for 2025

The IRS has announced increased HSA contribution limits for 2025, reflecting the government’s recognition of rising healthcare costs. For 2025, individuals with self-only High Deductible Health Plan (HDHP) coverage can contribute up to $4,300, while those with family coverage can contribute up to $8,550.

Participants aged 55 and older benefit from additional catch-up contributions of $1,000, bringing their total potential contributions to $5,300 for individual coverage and $9,550 for family coverage. These limits represent meaningful increases from 2024, providing more opportunity to build substantial healthcare reserves.

The tax benefits multiply the value of these contributions significantly. Every dollar contributed reduces your current tax burden, while growth within the account remains completely tax-sheltered. When you eventually use funds for qualified medical expenses, withdrawals are entirely tax-free, creating a powerful wealth preservation strategy.

Strategic HSA Usage for Current Healthcare Costs

Many people underutilize their HSAs by only thinking of them as emergency medical funds. Smart HSA management involves understanding how to optimize both current healthcare expense management and long-term growth potential.

For immediate healthcare needs, HSAs cover a comprehensive range of qualified expenses including:

- Deductibles and copayments for medical, dental, and vision care

- Prescription medications and over-the-counter items with prescriptions

- Medical equipment and supplies

- Certain preventive care services

- Mental health and substance abuse treatment

However, if your current financial situation allows, consider paying out-of-pocket for routine medical expenses while allowing your HSA to grow. This strategy, sometimes called “HSA investing,” maximizes the long-term compound growth potential of your account.

Long-Term HSA Investment Strategies for Retirement Healthcare

The most powerful HSA strategy involves treating your account like a specialized retirement fund dedicated to healthcare expenses. Research from the Plan Sponsor Council of America shows that HSA investment assets increased by 38% in 2024, reaching $64 billion, demonstrating growing recognition of HSAs’ long-term benefits.

Many HSA providers allow investment options once your account reaches certain balance thresholds, typically between $1,000 to $2,500. These investment options often include:

- Low-cost index funds tracking broad market indices

- Target-date funds appropriate for retirement planning

- Bond funds for more conservative growth

- International and sector-specific investment options

When considering HSA investment strategies, think about your timeline and risk tolerance. If you’re planning to use funds for current healthcare expenses, maintaining cash or cash-equivalent investments makes sense. However, if you can afford to let your HSA grow for decades, more aggressive investment allocations may be appropriate.

HSAs vs Other Healthcare Savings Options

Comparing HSAs to alternative healthcare savings approaches highlights their unique advantages. Traditional savings accounts offer liquidity but no tax benefits. Flexible Spending Accounts (FSAs) provide tax deductions but require annual spending of contributions or forfeiture.

HSAs combine the best features of both approaches while eliminating their limitations. Unlike FSAs, HSA funds roll over indefinitely, allowing you to build substantial balances over time. Unlike traditional savings, every aspect of HSA usage provides tax advantages when used appropriately.

For families evaluating healthcare savings options, HSAs often prove superior to increasing traditional retirement account contributions. While both strategies reduce current taxes, only HSAs provide completely tax-free distributions for healthcare expenses, which become increasingly important as healthcare costs consume larger portions of retirement budgets.

Real-World HSA Success Stories

Consider Sarah, a 35-year-old marketing manager who began maximizing her HSA contributions five years ago. Despite having relatively low healthcare expenses, she chose to pay routine medical costs out-of-pocket while investing her HSA funds in broad market index funds. Her account has grown from initial contributions of $3,500 annually to a current balance exceeding $25,000.

“I realized that healthcare costs were going to be one of my biggest retirement expenses,” Sarah explains. “By treating my HSA like a specialized retirement account, I’m building a dedicated fund that will grow tax-free for the next 30 years.”

Another approach comes from Tom and Linda, a married couple in their early 50s who use their HSA as both a current expense management tool and long-term investment vehicle. They maintain a cash balance sufficient for their typical annual healthcare expenses while investing the remainder for long-term growth.

“We track our healthcare expenses carefully and keep enough cash in the HSA to cover our usual costs,” Tom notes. “Everything above that threshold gets invested. It’s like having two accounts in one – immediate access for current needs and growth for future expenses.”

Maximizing HSA Benefits for Healthcare Cost Management

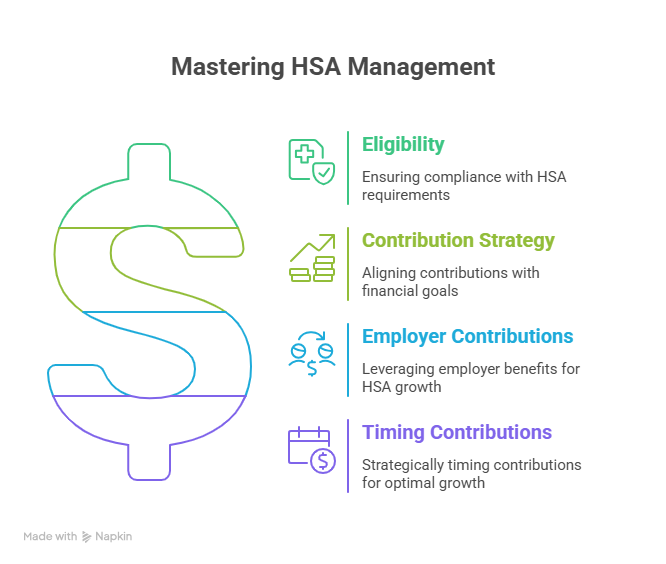

Effective HSA management requires understanding both the rules and optimal strategies for your situation. First, ensure you’re eligible by maintaining qualifying High Deductible Health Plan coverage without other disqualifying coverage.

Next, develop a contribution strategy aligned with your overall financial plan. If your employer offers HSA contributions or matching, prioritize capturing any free money. Many employers provide HSA contributions as part of their benefits package, essentially giving you additional compensation that grows tax-free.

Consider timing your contributions strategically throughout the year. While you can contribute the full annual limit at any time, spreading contributions allows for dollar-cost averaging if you’re investing HSA funds. Some people prefer to maximize contributions early in the year to extend the tax-free growth period.

Record Keeping and Expense Management

Proper HSA administration requires maintaining detailed records of all contributions, distributions, and qualified expenses. Many HSA providers offer online platforms that simplify tracking, but ultimate responsibility for compliance remains with the account holder.

Save receipts for all medical expenses, even those you pay out-of-pocket rather than reimbursing from your HSA. These receipts can justify future HSA withdrawals years or even decades later, providing flexibility in managing your tax-advantaged healthcare fund.

Consider using dedicated credit cards or payment methods for medical expenses to simplify tracking. Some HSA providers offer debit cards linked directly to your account, while others provide mobile apps that streamline expense documentation and reimbursement processes.

HSAs in Comprehensive Retirement Planning

Healthcare expenses represent one of the largest and most unpredictable categories of retirement spending. Merrill Lynch research on retirement planning emphasizes that healthcare costs often rise faster than general inflation, making dedicated planning essential for financial security.

HSAs integrate seamlessly with other retirement planning strategies. Unlike traditional IRAs or 401(k) accounts, HSAs don’t require minimum distributions, allowing your healthcare fund to continue growing as long as needed. After age 65, you can also use HSA funds for non-medical expenses (subject to ordinary income tax), providing additional retirement income flexibility.

The account portability makes HSAs particularly valuable for people who change jobs frequently or become self-employed. Unlike employer-sponsored FSAs or some retirement plans, your HSA remains entirely yours regardless of employment changes, ensuring continuity in your healthcare savings strategy.

Estate Planning Considerations for HSAs

HSAs offer unique estate planning benefits often overlooked in discussions of healthcare savings. If you name your spouse as your HSA beneficiary, the account transfers to them upon your death, maintaining its tax-advantaged status. This feature provides continuity for surviving spouses facing potentially significant healthcare expenses.

For non-spouse beneficiaries, HSAs become taxable income, but beneficiaries can reduce this tax burden by paying the deceased’s qualifying medical expenses within one year of death. This provision allows families to maximize the tax benefits even in difficult circumstances.

Common HSA Mistakes to Avoid

Several common errors can reduce HSA effectiveness or create tax complications. First, avoid using HSA funds for non-qualified expenses before age 65, as this triggers both income tax and a 20% penalty. Even small mistakes can become costly when discovered during tax preparation.

Don’t overlook HSA investment options if your provider offers them. Many people leave substantial HSA balances in low-yield cash accounts, missing significant growth opportunities. Review your provider’s investment options and consider allocating appropriate portions of your balance to growth-oriented investments.

Failing to maximize employer HSA contributions represents another missed opportunity. If your employer contributes to your HSA or offers matching contributions, ensure you’re capturing these benefits as part of your overall compensation package.

Avoiding Over-Contribution Penalties

HSA contribution limits are strict, and exceeding them creates tax complications. If you have HSA coverage for only part of the year, your contribution limit must be prorated accordingly. The IRS provides specific calculations for partial-year coverage that must be followed precisely.

Similarly, if you turn 65 mid-year and enroll in Medicare, your HSA contribution eligibility ends on your Medicare enrollment date. Plan these transitions carefully to avoid inadvertent over-contributions that require correction and potential penalties.

Advanced HSA Strategies for High Earners

High-income individuals can use HSAs as part of sophisticated tax planning strategies. Because HSA contributions reduce adjusted gross income, they can help high earners avoid or reduce exposure to various income-based tax provisions.

For business owners or self-employed individuals, HSAs provide additional flexibility. Self-employed people can generally deduct HSA contributions as business expenses, while still receiving all the standard HSA tax benefits. This double benefit makes HSAs particularly attractive for entrepreneurs and freelancers.

Some high earners use HSAs as part of tax diversification strategies in retirement. By maintaining traditional tax-deferred accounts, Roth accounts, and HSAs, retirees can optimize their tax burden by strategically choosing which accounts to tap for different types of expenses.

The Future of HSAs and Healthcare Policy

Healthcare policy continues evolving, but HSAs have shown remarkable staying power across different political administrations. The bipartisan appeal of HSAs stems from their market-based approach to healthcare cost management combined with meaningful tax benefits for savers.

Recent trends suggest expanding HSA eligibility and increasing contribution limits. Some policy proposals would allow HSAs to cover additional expenses like fitness memberships, nutritional supplements, and alternative medicine treatments. While these changes remain proposals, they indicate growing recognition of HSAs’ value in comprehensive healthcare planning.

Technology improvements continue making HSAs more user-friendly and accessible. Mobile apps, integration with health insurance systems, and simplified expense tracking reduce administrative burdens that previously limited HSA adoption.

Frequently Asked Questions About HSAs and Healthcare Costs

Can I contribute to an HSA if I’m covered by Medicare? No, Medicare enrollment makes you ineligible for HSA contributions. However, you can continue using existing HSA funds for qualified medical expenses throughout your lifetime.

What happens to my HSA if I change jobs? Your HSA is completely portable and remains yours regardless of employment changes. You can continue contributing if your new employer offers qualifying HDHP coverage, or simply maintain the existing account balance.

Can I invest HSA funds in the stock market? Most HSA providers offer investment options once your account reaches certain balance thresholds. Investment choices typically include mutual funds, index funds, and sometimes individual securities.

Are there any restrictions on when I can use HSA funds? You can withdraw HSA funds for qualified medical expenses at any time without taxes or penalties. The expenses must be incurred after your HSA was established, but there’s no requirement to use funds immediately.

How do HSAs compare to traditional retirement accounts for healthcare planning? HSAs offer superior tax treatment for healthcare expenses because withdrawals are completely tax-free for qualified uses. Traditional retirement accounts require paying income tax on all withdrawals, making them less efficient for healthcare expenses.

Health Savings Accounts represent one of the most powerful tools available for managing rising healthcare costs throughout your lifetime. By understanding contribution limits, investment strategies, and integration with broader financial planning, you can build substantial healthcare reserves while reducing your overall tax burden.

The combination of immediate tax deductions, tax-free growth, and tax-free qualified withdrawals creates a unique opportunity to protect yourself against one of retirement’s most significant and unpredictable expense categories. As healthcare costs continue rising faster than general inflation, the value of dedicated healthcare savings becomes increasingly important for long-term financial security.

Whether you’re just beginning your career or approaching retirement, incorporating HSA strategies into your financial plan can provide both peace of mind and substantial economic benefits. The key lies in understanding your options, maximizing available tax advantages, and maintaining consistent contributions that grow over time into meaningful healthcare security.