How to Build an Emergency Fund on a Tight Budget

If your budget already feels stretched, the phrase “build an emergency fund” can sound almost insulting. Save three to six months of expenses? With what money? That advice may be technically correct, but it does not help much when groceries, rent, insurance, utilities, and debt payments are already competing for the same paycheck.

The good news is that an emergency fund does not have to start big to be useful. A small cash cushion can still protect you from overdraft fees, credit card debt, payday loans, late payment penalties, and the stress spiral that comes with every surprise bill. The first goal is not perfection. The first goal is breathing room.

This guide walks through a realistic emergency fund plan for people who are saving on a tight budget. You will learn how much to save first, where to keep the money, how to find small amounts without wrecking your life, and how to rebuild the fund after you use it. This is general education, not personalized financial advice, but the framework can help you build a plan that fits your actual income and expenses.

What Is an Emergency Fund?

An emergency fund is money set aside for unexpected expenses or financial shocks. The Consumer Financial Protection Bureau describes it as a cash reserve for unplanned expenses such as car repairs, medical bills, home repairs, or income loss. In plain English, it is the money that keeps a bad day from becoming a long-term financial setback.

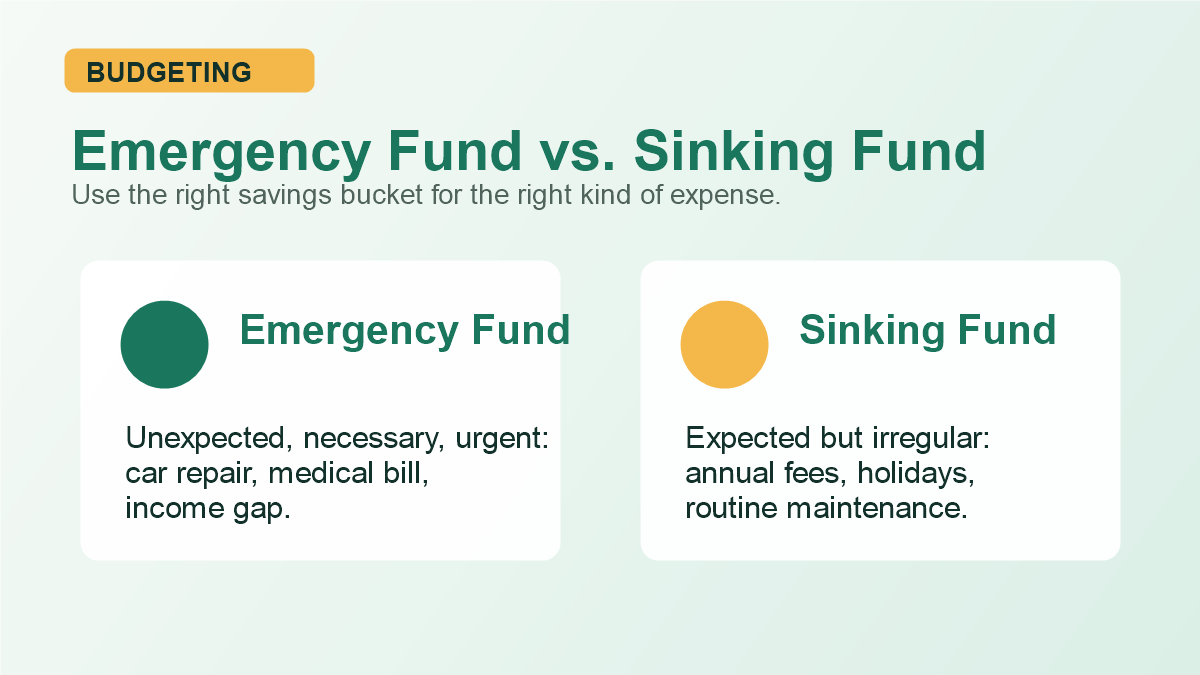

An emergency fund is not the same as a vacation fund, holiday fund, investing account, or “maybe I will buy something fun” account. It has a specific job: protect your monthly budget from surprises.

Common Emergency Fund Uses

- A car repair you need in order to get to work

- An urgent medical, dental, or vision bill

- A temporary loss of income or reduced work hours

- A necessary home repair, such as a broken appliance

- A last-minute travel need for a family emergency

- An insurance deductible after an accident

The key word is necessary. An emergency fund is for expenses that are urgent, important, and hard to delay. It is not for predictable bills that happen every year. Those need sinking funds, which we will cover later.

Why a Small Emergency Fund Still Matters

Many people skip saving because they cannot save a large amount. That is understandable, but it creates a trap. If you wait until you can save hundreds of dollars at a time, you may never start. Meanwhile, one $300 surprise can push you into credit card debt, overdraft fees, or missed payments.

The first emergency fund milestone is not three to six months of expenses. For many households, a starter emergency fund of $250, $500, or $1,000 is more realistic and more motivating. It will not solve every crisis, but it can absorb many common setbacks.

Think of emergency savings like a financial shock absorber. A shock absorber does not remove every bump in the road. It reduces the damage.

How Much Should You Save First?

The traditional rule of thumb is three to six months of essential expenses. That is still a useful long-term target, especially if your income is irregular, your job is less stable, or you have dependents. But if your budget is tight, start with smaller milestones.

| Milestone | Best For | What It Can Cover |

|---|---|---|

| $100 | Getting started | Small copays, school costs, minor bill timing gaps |

| $250 | Early cushion | Utility surprises, basic car issues, urgent household needs |

| $500 | Starter emergency fund | Many common repairs, deductibles, and short income gaps |

| $1,000 | Stronger first target | Larger repairs, medical bills, and several smaller emergencies |

| 1 month of expenses | Stability phase | Rent or mortgage, food, utilities, transport, insurance |

| 3 to 6 months | Long-term security | Job loss, major income disruption, extended emergencies |

If you currently have $0 saved, your first goal is $100. Once you reach $100, aim for $250. Then $500. Then $1,000. Each milestone gives you a win, which matters because money habits are easier to keep when you can see progress.

Step 1: Define What Counts as an Emergency

Before you save the money, decide what the money is allowed to do. This protects your emergency fund from slow leaks.

A simple rule is the three-part test:

- Is it unexpected? The expense was not part of your normal monthly budget.

- Is it necessary? Delaying it would create a bigger problem.

- Is it urgent? You need to handle it soon, not someday.

A broken tire that keeps you from getting to work passes the test. A sale on a new phone does not. A surprise medical bill may pass the test. A birthday gift you forgot to budget for is real, but it is not exactly an emergency. That belongs in a separate short-term savings bucket.

Step 2: Pick a Starter Goal That Does Not Feel Impossible

If your first target is too large, your brain may treat it like fantasy. Make it concrete and reachable. For example:

- “I am saving my first $100 in 30 days.”

- “I am saving $250 before I make extra debt payments.”

- “I am saving $500 by setting aside $20 from each paycheck and one extra cash boost per month.”

Do not compare your starter fund to someone else’s six-month cash reserve. Your first emergency fund is not a status symbol. It is a tool.

Step 3: Open a Separate Savings Account

Keeping emergency money in your everyday checking account makes it too easy to spend by accident. A separate savings account creates helpful friction. You can still access the money when you truly need it, but it is not sitting beside your grocery and gas money.

The FDIC explains that savings accounts are generally used to set aside money for future needs, while checking accounts are designed for frequent transactions. That difference is exactly why a savings account can work well for emergency money.

Look for an account with:

- No monthly maintenance fee

- No minimum balance that creates pressure

- Easy transfers from your checking account

- FDIC or NCUA insurance through a bank or credit union

- A little separation from your normal spending account

A high-yield savings account can be useful, but do not let rate shopping delay the habit. The behavior matters more than squeezing out a tiny amount of extra interest on your first $100.

Step 4: Build a Tiny Automatic Transfer

Automation is powerful because it removes the monthly debate. Even $5 or $10 per paycheck can build momentum. If that sounds too small, remember that $10 every two weeks becomes $260 in a year. Add one tax refund boost, cash-back reward, side gig payment, or unused subscription cancellation, and the fund grows faster.

Start with an amount you can keep. A tiny transfer that actually happens is better than an ambitious transfer you cancel after two weeks.

Starter Automation Ideas

- $5 every Friday

- $10 every payday

- 1 percent of each paycheck

- Round up purchases and move the difference weekly

- Save the first $25 of any extra income

If your income is irregular, use a percentage instead of a fixed amount. For example, save 3 percent of each deposit until you reach $500. When the check is smaller, the transfer is smaller. When the check is larger, you make more progress.

Step 5: Find the First $100 Without Feeling Deprived

When money is tight, the problem is not usually that you are wasting huge amounts. Often, the budget is already lean. So the goal is not to shame yourself into saving. The goal is to find small pressure-release points.

Start with a one-week money scan. Look through the last seven days of spending and ask three questions:

- Was anything accidental, duplicated, or forgotten?

- Was anything convenient but not worth the cost?

- Is there one expense I would pause for 30 days to buy financial peace?

You might find an unused subscription, a delivery fee habit, bank fees, an impulse shopping pattern, or a grocery item that keeps getting thrown away. You do not need to overhaul your whole life. You need the first $100.

If impulse spending is part of the challenge, your existing guide on the no-buy challenge can pair well with this emergency fund plan. A short no-buy period works best when the money saved is moved immediately into a separate account.

Step 6: Use Cash Boosts Strategically

Small automatic transfers create consistency. Cash boosts create speed. A cash boost is any money outside your normal monthly income that can help you reach your starter goal faster.

Examples include:

- Tax refunds

- Work bonuses

- Reimbursements

- Cash gifts

- Marketplace sales

- Credit card cash-back rewards

- Extra paycheck months

- Side hustle income

You do not have to save 100 percent of every cash boost. A balanced rule can work better. For example, save 70 percent, use 20 percent for urgent needs, and keep 10 percent for something enjoyable. That way, saving does not feel like punishment.

Step 7: Separate Emergencies From Predictable Irregular Bills

One reason emergency funds fail is that they get used for expenses that are predictable but not monthly. Car registration, annual insurance premiums, holiday gifts, school supplies, and routine maintenance are not surprises. They are irregular bills.

The fix is to create sinking funds. A sinking fund is money saved gradually for a known future expense. If car registration costs $240 once a year, save $20 per month. If holiday spending usually costs $600, save $50 per month. This keeps your emergency fund from doing every job in your financial life.

Your emergency fund should handle the unexpected. Your sinking funds should handle the expected-but-infrequent.

Step 8: Decide Whether to Save or Pay Debt First

If you have high-interest debt, it can feel strange to save cash while interest is building. But having no emergency fund can push you deeper into debt the next time something goes wrong.

A practical approach is:

- Save a starter emergency fund of $250 to $1,000.

- Keep making required minimum debt payments.

- After the starter fund is in place, attack high-interest debt more aggressively.

- Once the debt is under better control, build toward one month of expenses.

This is not a one-size-fits-all rule. If you are behind on rent, utilities, taxes, or secured debt, those priorities may come first. But for many people, a small emergency fund makes debt payoff more stable because it reduces the need to borrow again.

If credit card debt and credit score stress are part of the picture, read your guide on how to improve your credit score. Emergency savings and credit health often support each other because cash helps you avoid missed payments and new balances.

Step 9: Create a Bare-Bones Budget Number

Eventually, you want your emergency fund to cover essential expenses, not your full lifestyle. To calculate one month of bare-bones expenses, add only the bills you would need to survive a temporary income drop.

| Essential Category | Include | Usually Exclude |

|---|---|---|

| Housing | Rent, mortgage, basic utilities | Decor, upgrades, nonurgent repairs |

| Food | Groceries and basic household items | Restaurants, delivery, premium extras |

| Transportation | Gas, transit, insurance, required repairs | Road trips, upgrades, convenience rides |

| Debt | Minimum payments | Extra payments during crisis mode |

| Health | Insurance, prescriptions, necessary care | Optional wellness spending |

If your bare-bones number is $2,800, then one month of emergency savings is $2,800. Three months is $8,400. That may feel big, but you do not have to reach it at once. Your first $500 still counts.

Step 10: Protect the Fund From Lifestyle Creep

Once your emergency fund starts growing, you may feel tempted to relax other parts of your budget. That is normal. Progress can make money feel less urgent. The trick is to create a few guardrails.

- Name the account something specific, such as “Emergency Only.”

- Keep it separate from checking.

- Review it monthly, not daily.

- Write down the three-part emergency test.

- Refill it immediately after using it.

If you share finances with a partner, agree on the rules before an emergency happens. Decide what dollar amount requires a conversation and what types of expenses automatically qualify.

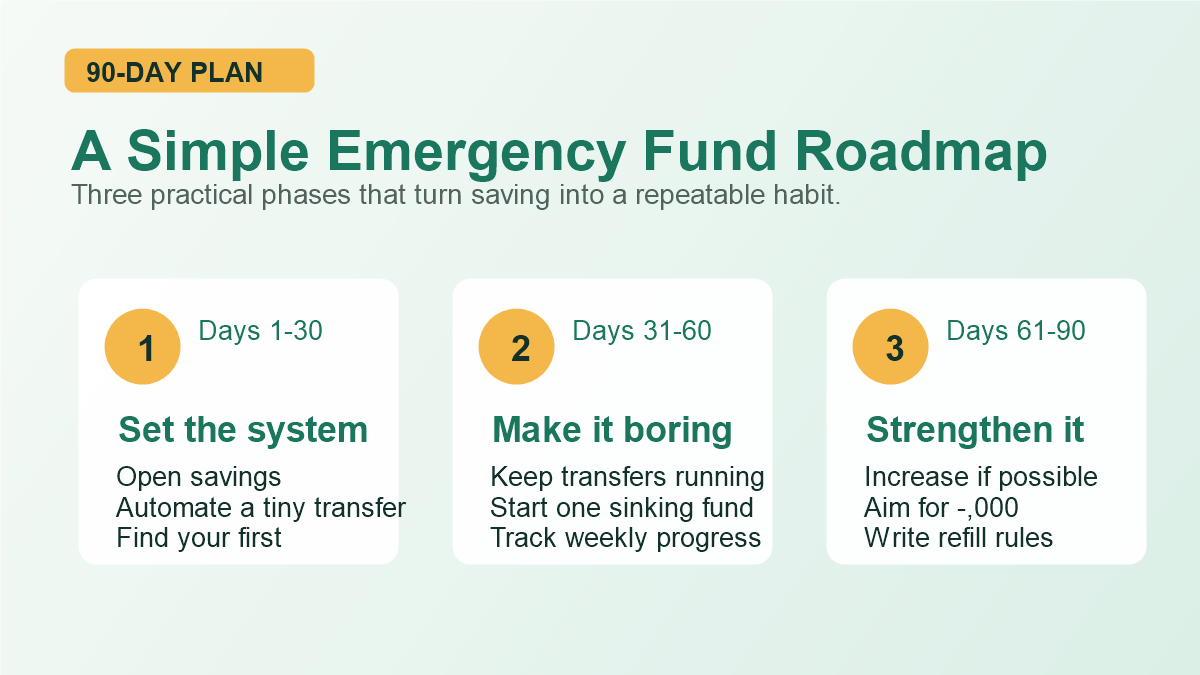

A Simple 90-Day Emergency Fund Plan

Here is a starter plan you can use even if your budget is tight.

Days 1 to 7: Set Up the System

- Open or choose a separate savings account.

- Set your first target: $100, $250, or $500.

- Create one tiny automatic transfer.

- Review the last week of spending for one quick savings opportunity.

Days 8 to 30: Reach the First Win

- Move any found money into savings immediately.

- Cancel or pause one low-value recurring expense.

- Try one no-spend weekend or pantry week.

- Sell one unused item if you have something easy to list.

Days 31 to 60: Make It Boring

- Keep the automatic transfer running.

- Start one sinking fund for a predictable irregular bill.

- Review progress once per week.

- Move extra income using a percentage rule.

Days 61 to 90: Strengthen the Habit

- Increase the transfer slightly if the first amount feels easy.

- Build toward $500 or $1,000.

- List your top three likely emergencies and estimate their cost.

- Decide your next milestone after the starter fund is complete.

For additional saving ideas, connect this plan with your article on how to save money with strategies that actually work. The best emergency fund plan is usually not one dramatic sacrifice. It is a system of small choices that repeat.

What If You Have to Use the Emergency Fund?

Using the fund is not failure. It is the reason the fund exists. If you use $300 to fix your car and avoid missing work, the emergency fund did its job.

After you use it:

- Pause and confirm the expense was a true emergency.

- Update your balance.

- Restart your automatic transfer.

- Temporarily direct extra cash toward rebuilding.

- Ask whether a sinking fund could prevent a similar withdrawal next time.

The goal is not to never touch the money. The goal is to avoid turning every surprise into debt.

Emergency Fund Mistakes to Avoid

Waiting Until You Can Save a Lot

Small savings count. A $10 transfer is not meaningless. It is a vote for stability, and repeated votes become a habit.

Keeping the Money Too Accessible

If the money sits in checking, it may disappear into normal spending. Use a separate account so the money has a clear job.

Investing Your Emergency Fund

Your emergency fund should be stable and accessible. Investing is important for long-term growth, but emergency savings should not be exposed to market swings when you may need it quickly.

Using It for Non-Emergencies

Every withdrawal should pass the unexpected, necessary, and urgent test. If it does not, create a different savings bucket.

Stopping After the First Goal

Reaching $500 or $1,000 is worth celebrating, but it is not the end. After the starter fund, build toward one month of essential expenses, then three months, then more if your life calls for it.

FAQ: Building an Emergency Fund on a Tight Budget

Is $500 enough for an emergency fund?

$500 is not enough for every emergency, but it is a useful starter fund. It can cover many smaller surprises and reduce the need to borrow. After reaching $500, consider building toward $1,000 and then one month of essential expenses.

Should I save an emergency fund if I live paycheck to paycheck?

Yes, if you can save even a small amount. Paycheck-to-paycheck households often benefit the most from a cash cushion because one surprise can create late fees, overdrafts, or new debt. Start with a tiny automatic transfer and a realistic first milestone.

Where should I keep my emergency fund?

A separate savings account at an insured bank or credit union is usually a practical choice. The money should be accessible for real emergencies but separate enough that you do not spend it accidentally.

Should I pay off debt or build emergency savings first?

Many people benefit from saving a small starter emergency fund while making required debt payments. After that, you can focus more aggressively on high-interest debt. Your best order depends on your income, debt type, and whether you are current on essential bills.

How do I rebuild my emergency fund after using it?

Treat rebuilding as the next emergency. Restart automatic transfers, send extra cash boosts to the account, and pause lower-priority spending until your starter balance is restored.

Final Takeaway

Building an emergency fund on a tight budget is not about suddenly finding hundreds of extra dollars. It is about creating a small, repeatable system that protects you before life gets expensive again.

Start with $100. Keep it separate. Automate a tiny transfer. Use cash boosts when they appear. Protect the fund with clear rules. Then build the next milestone. The first step may feel small, but it changes the direction of your financial life.

For more ways to strengthen your money foundation, explore your guides on proven money-saving strategies and money trends shaping financial decisions.