Hidden Costs of Buying a House: Beginner Budget Guide

Buying a house is exciting because the goal is easy to picture: keys in your hand, your own front door, and a place that feels more stable than renting. But the math can get blurry fast. Many first-time buyers focus on the down payment and the monthly mortgage payment, then get surprised by closing costs, insurance, property taxes, repairs, moving costs, and the steady stream of small purchases that show up after move-in day.

The hidden costs of buying a house are not always hidden because someone is trying to trick you. They are hidden because they arrive in different documents, at different stages, and from different companies. The lender talks about loan costs. The title company talks about settlement charges. The insurance company has its own quote. The inspector may uncover repairs. The moving company has another invoice. Then the first utility bill arrives.

This guide is designed to help beginner homebuyers build a more realistic homebuying budget before making an offer. It is general education, not personalized mortgage, legal, tax, or investment advice. Your exact costs depend on your location, loan type, lender, property, contract terms, insurance needs, and local taxes. But the framework below will help you ask better questions and avoid becoming house poor immediately after closing.

Why the Purchase Price Is Only the Starting Point

The listing price tells you what the seller wants for the home. It does not tell you the full cost of buying, financing, owning, moving into, and maintaining that home. A buyer who can technically afford the mortgage payment may still feel squeezed if the rest of the costs are ignored.

Think of the home purchase in four layers:

- Upfront cash: down payment, closing costs, prepaid items, escrow deposits, inspections, appraisal, and moving money.

- Monthly housing costs: mortgage principal and interest, property taxes, homeowners insurance, mortgage insurance, HOA dues, and utilities.

- First-year setup costs: repairs, tools, furniture gaps, locks, safety items, appliances, lawn care, and deposits.

- Long-term ownership costs: maintenance, replacements, insurance changes, tax changes, and emergency repairs.

A strong homebuying budget looks at all four. If you only look at the mortgage payment, you are budgeting for the loan, not the home.

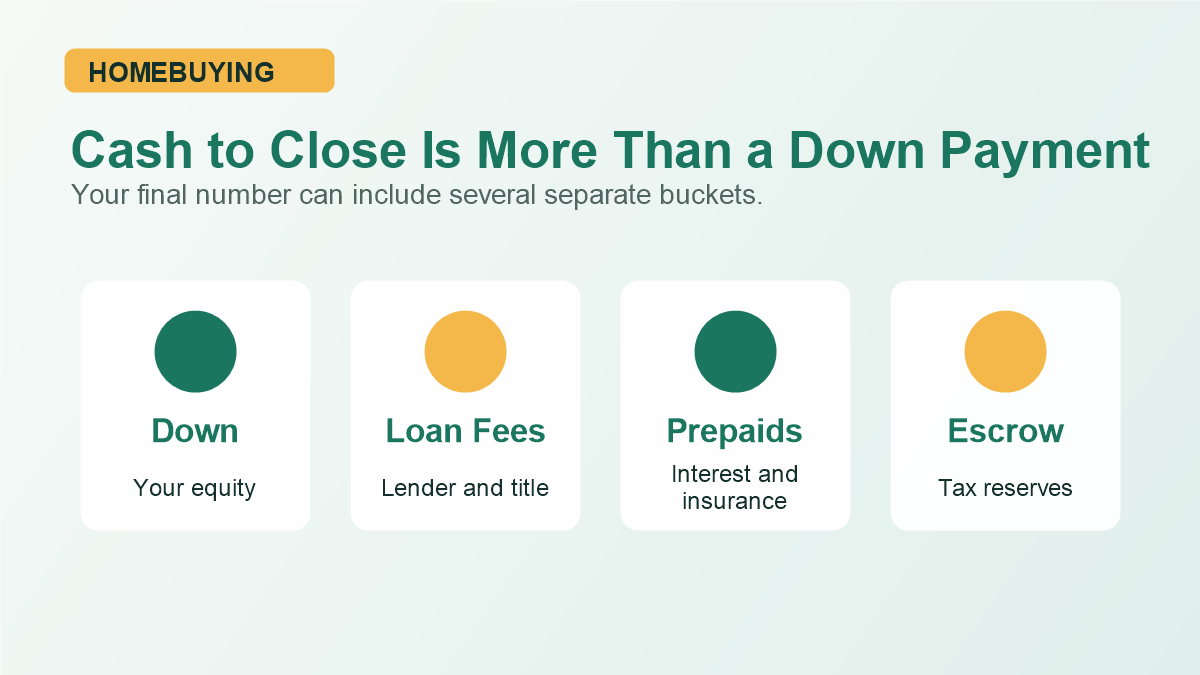

1. Closing Costs

Closing costs are the fees and expenses paid to finalize the purchase and mortgage. The Consumer Financial Protection Bureau explains that these fees may be paid directly or indirectly, depending on the loan structure and lender credits. In practical terms, buyers should not assume a “no closing cost” loan means the cost disappears. It may be built into the loan amount or interest rate.

Common closing cost categories include:

- Lender origination charges

- Discount points, if you choose to pay them

- Appraisal fee

- Credit report fee

- Title search and title insurance

- Settlement or closing agent fees

- Recording fees and transfer taxes where applicable

- Attorney fees in states where attorneys are commonly used

The exact mix varies. This is why comparing lenders only by the monthly payment can be misleading. Two loans can have similar payments but very different upfront costs.

2. Prepaid Costs and Escrow Deposits

Prepaids are costs you pay at closing for expenses that begin right away, such as prepaid interest, homeowners insurance, or property tax reserves. Escrow deposits are funds collected so your mortgage servicer has money available for future tax and insurance bills if those items are escrowed.

These costs can surprise buyers because they are not exactly “fees.” You may be paying for real expenses you would owe anyway. But they still affect how much cash you need to bring to closing.

The CFPB’s Closing Disclosure explainer highlights areas buyers should review, including estimated taxes, insurance, assessments, closing costs, and cash to close. That document is one of the most important tools for spotting the difference between the number you expected and the number you must actually pay.

3. Home Inspection and Follow-Up Inspections

A general home inspection is one of the most useful expenses in the buying process. HUD encourages homebuyers to consider a professional inspection because it can reveal problems that are not obvious during a showing. The inspection does not guarantee a perfect house, but it can help you make a better decision before closing.

Some buyers also need specialized inspections based on the home and region:

- Termite or pest inspection

- Sewer scope

- Roof inspection

- Foundation inspection

- Radon testing

- Well or septic inspection

- Chimney inspection

The mistake is budgeting for only the general inspection and assuming that is the end. If the inspector flags a major issue, you may need a specialist to estimate the repair. That can cost more upfront, but it may save you from buying a problem you do not understand.

4. Appraisal Gaps

If you are using a mortgage, the lender usually wants an appraisal to help confirm the value of the home. If the appraisal comes in lower than the purchase price, you may face an appraisal gap. That means the lender may base the loan on the appraised value rather than the contract price.

For example, if you agree to pay ,000 and the appraisal comes in at ,000, the ,000 difference may need to be renegotiated, covered with additional cash, or handled another way under your contract terms. In a competitive market, buyers sometimes waive protections without fully understanding the risk.

Before making an offer, ask your agent and lender how appraisal gaps work in your market and how much cash you would realistically have available if the appraisal is low.

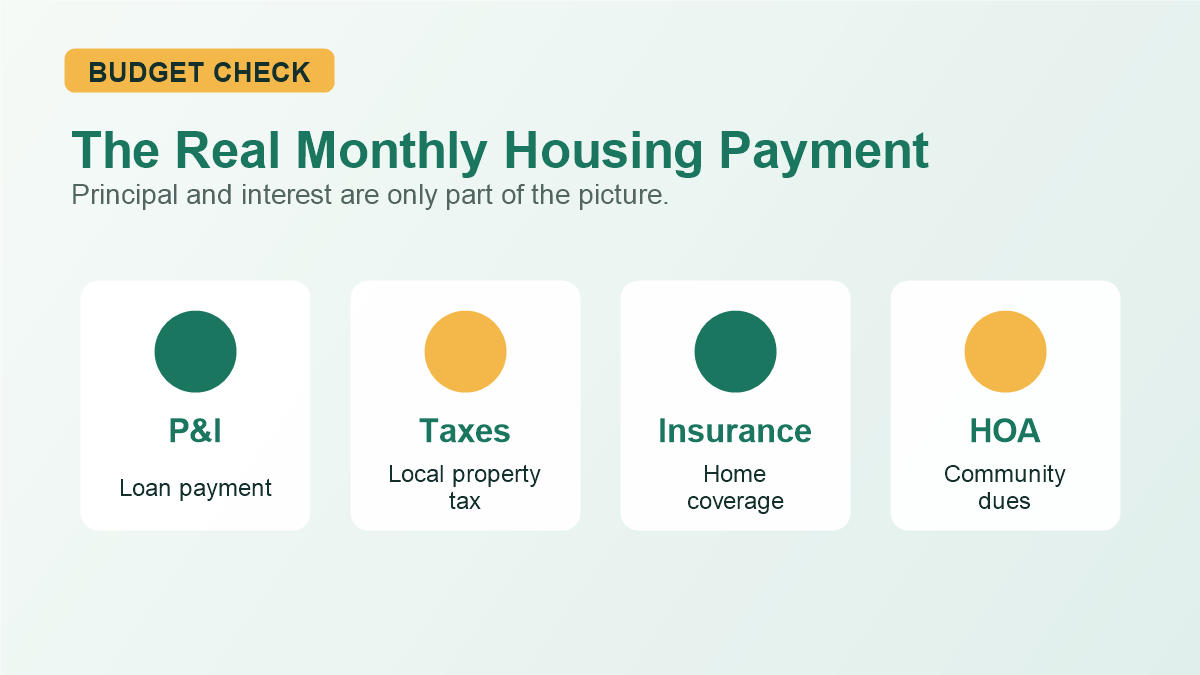

5. The Real Monthly Payment

Many buyers ask, “What will my mortgage payment be?” A better question is, “What will my total monthly housing cost be?” Principal and interest are only part of the monthly number.

Your full housing payment may include:

- Mortgage principal and interest

- Property taxes

- Homeowners insurance

- Mortgage insurance, depending on your loan and down payment

- HOA or condo dues

- Utilities

- Trash, water, sewer, or local service fees

- Routine maintenance savings

Property taxes and insurance can also change over time. A payment that feels manageable at closing may feel different after an escrow analysis, insurance premium increase, or local tax reassessment.

6. HOA Dues and Special Assessments

Homeowners association dues can cover useful services, but they are still part of your housing cost. Condo and HOA communities may also have rules, reserves, and special assessments. A special assessment is an extra charge to owners for a major project or funding shortfall.

Before buying into an HOA or condo association, review the dues, rules, recent meeting notes if available, reserve funding, upcoming projects, and assessment history. A low monthly fee is not automatically good if the association is underfunded.

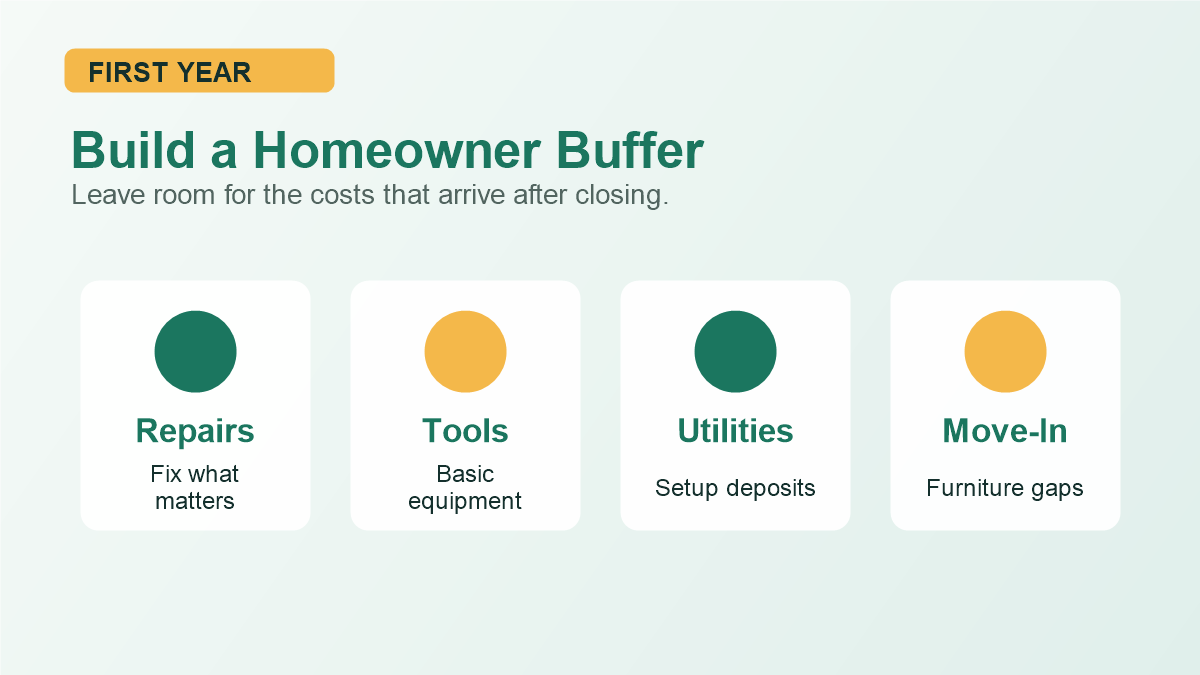

7. Moving and Move-In Costs

Moving is one of the easiest costs to underestimate because it feels separate from the home purchase. But it arrives at the same time your cash is already stretched.

Potential move-in costs include:

- Movers or truck rental

- Packing supplies

- Utility deposits or setup fees

- New locks or rekeying

- Basic tools

- Window coverings

- Cleaning supplies

- Furniture that does not fit the new space

- Lawn equipment or snow removal tools

The goal is not to buy everything right away. The goal is to keep enough cash available so the first month of ownership does not go straight onto a credit card.

8. Immediate Repairs

Even a well-maintained home can need attention soon after closing. Sellers may have lived with small issues for years. Once you own the home, those small issues become your list.

Examples include leaky faucets, missing safety equipment, loose railings, garage door service, HVAC tune-ups, appliance repairs, drainage fixes, and roof maintenance. None of these may be dramatic enough to stop the purchase, but together they can pressure your budget.

This is where your emergency fund matters. If you recently read our guide on building an emergency fund on a tight budget, the same principle applies to homeownership: small cash buffers prevent small problems from becoming expensive debt.

9. Maintenance and Replacement Costs

Renters often call a landlord when something breaks. Homeowners call a contractor, buy the part, or learn to fix it themselves. That shift is one of the biggest financial changes of owning a home.

Home maintenance includes routine care and eventual replacement. Think HVAC filters, gutter cleaning, landscaping, pest control, appliance repair, water heater replacement, roof maintenance, plumbing work, and exterior upkeep. Some years may be quiet. Other years may bring several repairs at once.

A beginner-friendly approach is to create a monthly home maintenance sinking fund. This is separate from your emergency fund. The emergency fund covers the unexpected. The maintenance fund prepares for the reality that houses age.

10. Insurance Gaps

Homeowners insurance is required by most lenders, but not every policy covers every risk. Depending on where you live, you may need to consider flood insurance, earthquake coverage, windstorm deductibles, sewer backup coverage, or higher personal property limits.

Do not shop insurance only by the lowest premium. Ask what the deductible is, what is excluded, whether replacement cost coverage applies, and what special risks are common in the area. A cheaper policy can become expensive if it leaves out the risk you actually face.

11. Utility Changes

A home may cost more to heat, cool, water, and maintain than your previous place. Larger square footage, older windows, inefficient appliances, irrigation, pool equipment, or local service fees can all raise monthly costs.

Before closing, ask for average utility costs when possible. They will not be perfect, because usage varies by household, but they can help you avoid guessing from scratch.

12. Opportunity Cost

Using most of your cash to buy a home can leave you vulnerable. If your down payment and closing costs drain your savings, you may own the house but lose flexibility. That can affect your ability to handle job changes, medical expenses, car repairs, or family needs.

A stronger plan leaves cash after closing. You do not need to be rich to buy responsibly, but you should avoid entering homeownership with no cushion at all.

A Practical Hidden-Cost Budget Checklist

Before making an offer, build a buyer budget with these lines:

| Cost Category | When It Appears | Why It Matters |

|---|---|---|

| Down payment | Closing | Determines equity and loan structure |

| Closing costs | Closing | Can materially change cash needed |

| Prepaids and escrow | Closing | Covers early tax, insurance, and interest items |

| Inspection costs | Before closing | Helps identify repair and safety issues |

| Moving costs | Move-in | Protects cash flow during the transition |

| First-year repairs | After closing | Reduces reliance on credit cards |

| Maintenance fund | Monthly | Prepares for normal ownership costs |

How to Avoid Becoming House Poor

Being house poor means the home payment technically fits on paper, but the rest of life becomes financially cramped. You may still be able to pay the mortgage, but saving, investing, emergencies, repairs, travel, child care, and normal life all become harder.

To reduce that risk:

- Compare total monthly housing cost, not just principal and interest.

- Review your Loan Estimate and Closing Disclosure carefully.

- Keep a cash cushion after closing.

- Budget for repairs before they happen.

- Do not ignore HOA dues, insurance deductibles, or utility changes.

- Run the numbers using a conservative income estimate.

- Delay nonessential upgrades until your savings recover.

If you are still early in the process, our first-time homebuyer guide can help you understand the broader roadmap. If you are comparing market conditions, the 2026 real estate market forecast adds context, but your personal budget still matters more than headlines.

FAQ: Hidden Costs of Buying a House

What is the biggest hidden cost of buying a house?

For many buyers, the biggest surprise is cash to close. It can include the down payment, closing costs, prepaid items, and escrow deposits. After closing, repairs and maintenance are often the next major surprise.

Are closing costs separate from the down payment?

Yes. The down payment is your upfront equity in the home. Closing costs are fees and expenses required to complete the transaction and mortgage. Both can affect your cash needed at closing.

Should I spend all my savings on a down payment?

Usually, it is risky to use every dollar of savings at closing. Homeownership comes with repairs, maintenance, and life surprises. Keeping a cash cushion can make the first year much more stable.

Can I negotiate closing costs?

Some costs may be negotiable, shopable, or covered through seller concessions depending on the market, loan type, and contract. Other costs, such as certain taxes or government recording fees, may be less flexible. Ask your lender and real estate agent which costs can be shopped or negotiated.

How much should I save for home maintenance?

There is no perfect number because homes vary by age, condition, size, and location. A practical starting point is to create a monthly maintenance sinking fund and increase it if the home is older, larger, or has major systems nearing replacement.

Final Takeaway

The hidden costs of buying a house are manageable when you plan for them early. The danger is not that closing costs, repairs, taxes, insurance, and moving expenses exist. The danger is pretending they will not affect your budget.

Before making an offer, look beyond the listing price and monthly mortgage estimate. Build a full buyer budget, review official mortgage documents carefully, keep cash after closing, and give your first year of ownership some breathing room. A home should support your financial life, not quietly consume every spare dollar.